Private Equity Cardiology in the Midwest. Here's What the Data Shows.

By Catharine Szefcyk, Causeway Solutions

For most of the past decade, private equity largely left cardiology alone. The specialty was seen as too complex, too physician-dependent, and too tightly affiliated with hospital systems to roll up cleanly. PE was busy consolidating ophthalmology, dermatology, gastroenterology, and dentistry.

That changed around 2019, when Centers for Medicare and Medicaid Services (CMS) began approving an expanding list of cardiovascular procedures for reimbursement in ambulatory surgery settings. After that, outpatient cardiology became a different financial proposition almost overnight, and PE moved quickly.

A 2024 Journal of the American College of Cardiology (JACC) report found more than 340 PE acquisitions of cardiology clinics between 2013 and 2023, with over 94% of them occurring between 2021 and 2023 alone. The first wave landed primarily in the South and West. Texas, Florida, Arizona, and Nevada saw the highest concentration of PE-acquired cardiology practices.

The Midwest was largely untouched during that first wave. Based on what the data shows, that may start to change.

The Second Wave: Why Ohio

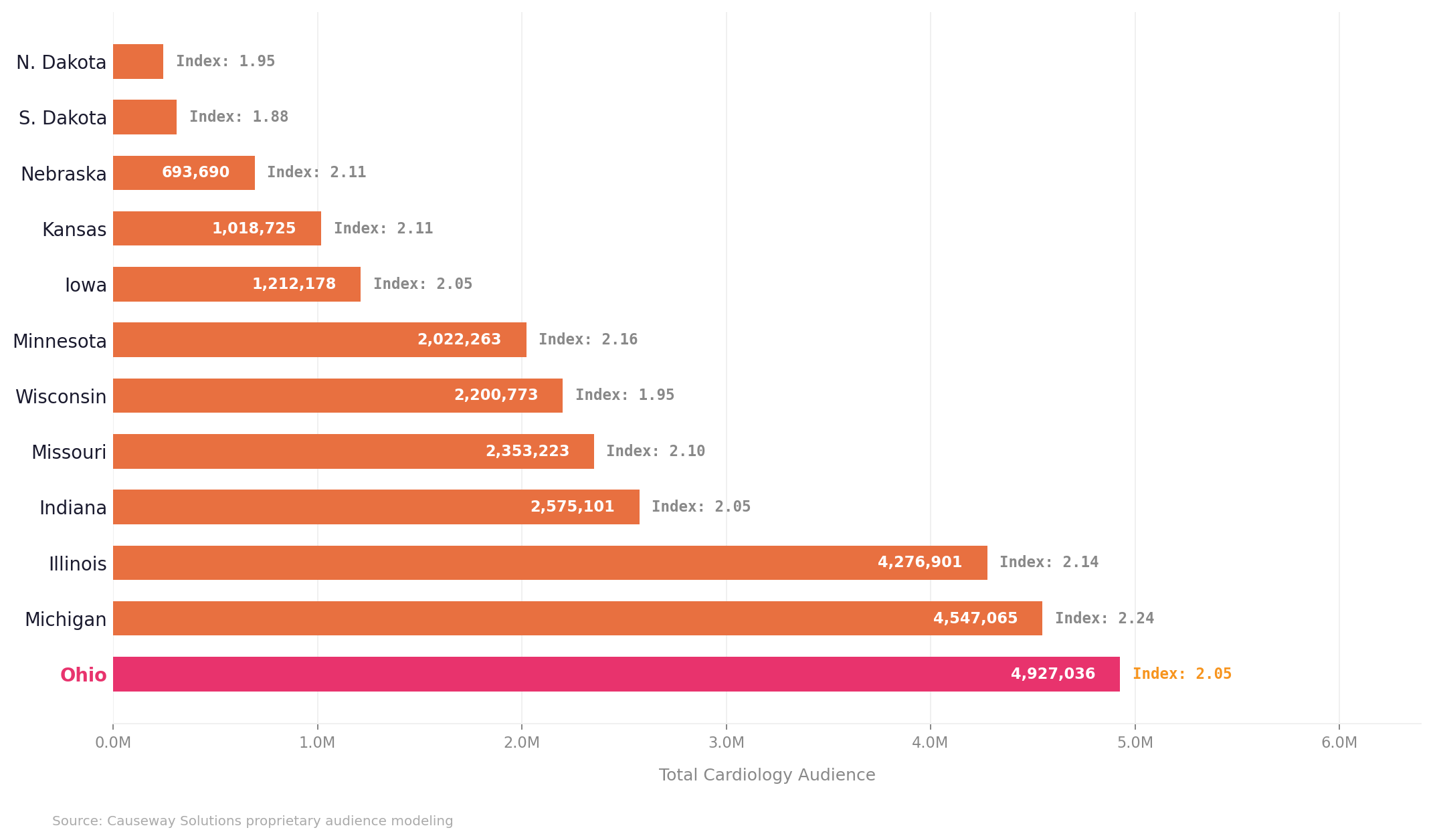

The next logical expansion targets share a common profile: large aging populations, high rates of cardiovascular disease, and substantial addressable cardiology patient populations. To understand where that opportunity is largest in the Midwest, we analyzed cardiology patient audiences across all 12 Midwest states.

Ohio has the largest addressable cardiology population in the region with nearly 5 million individuals with documented cardiac risk factors, low self-reported health status, and a high behavioral propensity to consult a cardiologist.

Midwest Cardiology Patient Opportunity by State

Total addressable audience with cardiac risk factors and propensity to consult a cardiologist

The Cardiology Index reflects the likelihood of this audience to seek cardiology care relative to the average person in each state. Data derived from Causeway Solutions proprietary audience modeling.

According to MedAxiom's 2024 Cardiovascular Provider Compensation and Production Survey, PE now owns nearly 50% of cardiology practices nationally, and the largest platforms are all in active acquisition mode. Independent cardiology practices in Ohio are potential acquisition targets, meaning the competitive set in these markets could shift quickly and without much public notice.

The competitive pressure this creates tends to arrive before health system leaders recognize its source. Volume softens in a particular geography and referral patterns shift slightly. By the time the trend is visible in the data, the competitor has already established patient relationships that are difficult to displace.

What the Data Shows

To understand what PE investors see in a market, health systems need to be looking at the same data.

Across three major Ohio DMAs, the cardiology patient opportunity is substantial. The Columbus DMA alone has 619,583 households with documented cardiac risk factors, low self-reported health status, and a high behavioral propensity to consult a cardiologist. The cardiology propensity index for this audience is 2.23, meaning they are more than twice as likely to seek cardiology care as the average Ohio resident. Cleveland-Akron-Canton has over one million cardiology opportunity households and Toledo adds nearly 289,000 more.

These are not abstract market estimates. They are scored, addressable populations built from behavioral and health propensity data at the individual level.

Franklin County, the core of the Columbus DMA, is the fastest-growing major county in Ohio. The 45 and older population is large and growing, commercially insured at a higher rate than Cleveland or Toledo, and represents a patient segment with both high cardiology need and favorable economics for a specialty practice. No single system owns the cardiology category in Columbus the way a nationally ranked competitor does in the Cleveland market. That combination of factors, a large addressable audience, favorable payer mix, and a fragmented competitive set, is exactly what a disciplined market entry looks like on paper.

That's why we went deeper on Columbus.

Healthcare Behaviors: Knowing Your Columbus Cardiology Patient

Not every market will look the same, so it is important to understand who your cardiology patients are, how they make care decisions, and reach them before someone else does.

Nearly 85% prefer to schedule medical appointments by phone. Not an app. Not a patient portal. A phone call. This is an audience that expects a human on the other end.

Nearly 55% are 65 and older, with Medicare and Medicare Advantage covering close to half. These are patients with established healthcare habits and existing provider relationships. They are not easily moved by a new name in the market. But they are not immovable either.

Connection is the top driver of care at 41.6%, ahead of both convenience and quality. They are looking for a provider they trust, and an established health system already has that. A PE-backed entrant is starting from zero. But that advantage closes fast once a competitor is in market and actively building those connections.

Source: Causeway Solutions Audience Intelligence Report: Cardiology Patient Opportunities, Columbus DMA. Data derived from proprietary audience modeling

What Health Systems Should Do With This

The most important thing health system marketing and strategy leaders can do right now is close the intelligence gap.

PE-backed entrants are making market selections based on data. But much of the underlying data driving these investor decisions comes from claims, which captures what care was delivered but is inherently backward-looking. The stronger move is selecting markets based on where cardiology demand is heading, not where it has been, not by simply chasing past case volume.

Four things worth acting on now-

Don't assume your brand will hold itself. Established health systems have something PE-backed entrants will spend years building: recognized, trusted provider brands in the community. But that advantage only holds if you stay proactive. High-risk patients who aren't actively engaged are exactly the ones a new entrant will reach first. Understanding who they are and how to reach them is how you keep your cardiology brand top of mind before they ever need care.

Know your addressable cardiology populationat the market level, not just the patients already in your system. Understanding that population, its size, location, behavioral profile, and channel preferences, is the starting point.

Audit your competitive white space honestly. In which geographies within your market are you genuinely strong? Where are you present but not deeply rooted? Where are you effectively absent?

Connect your audience intelligence to your media strategy. Knowing who the high-risk cardiology patients are in your market is only useful if your campaigns are actually reaching them. Your media strategy should be built on audience intelligence, not the other way around. Start with the data, then build the campaign around it.

The health systems best positioned to hold their ground are the ones applying the same quality of intelligence to their own markets that PE investors bring to market selection. The first wave happened in markets that were not paying close enough attention. The conditions for a second wave are already visible in the data. The question is whether Ohio health systems will see it before they feel it.

Causeway Solutions builds healthcare audience intelligence for health systems across the country. We help you understand your cardiology patient opportunity, identify where you're vulnerable, and build an activation and reach plan to get ahead of it.

We put together a sample Columbus DMA cardiology market brief showing what this intelligence looks like in practice. Email us at info@causewaysolutions.com for the report.