Causeway Solutions Outlooks and Insights: Volume 10, 06/22 - Instant Insights

Therese Mulvey

Analysis, Polling, Consumer Confidence

June 4, 2022

Better-Offs versus Worse-Offs: A Difference of Attitude

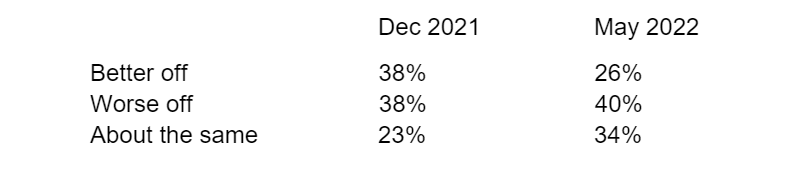

2022 has proven to be a less-than-stable year. As supply chain issues continue, interest rates increase, and the overall cost of living becomes less than optimal, we find that American consumers’ optimism is fighting to sustain. In December of last year, we asked people if they were better or worse financially than they were two years ago, and almost 40% responded they were better off. Only six months later and that number has dropped to only 26%. While those who say they are worse off have not changed that much, those who say they are about the same have risen from 23% to 34%.

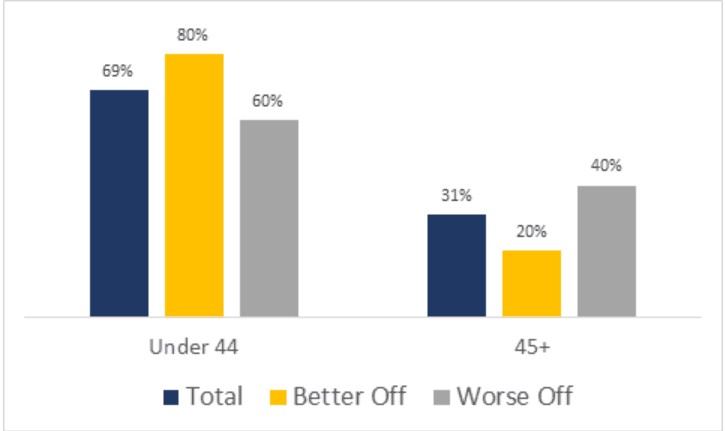

When we look deeper into the differences between these groups, we find that those who say they are about the same are often very similar to the average, but those who are better off are much more optimistic about almost everything. The “Better-Offs” are also more likely to be under 44, while the “Worse-Offs” are more likely to be over 45. Gender is also a factor, with women accounting for only 45% of the Better-Offs and 56% of the Worse-Offs.

Political differences also show up, and “Better-Offs” are more likely to be both progressive and democratic, while “Worse-Offs” are more likely to be republican and less progressive.

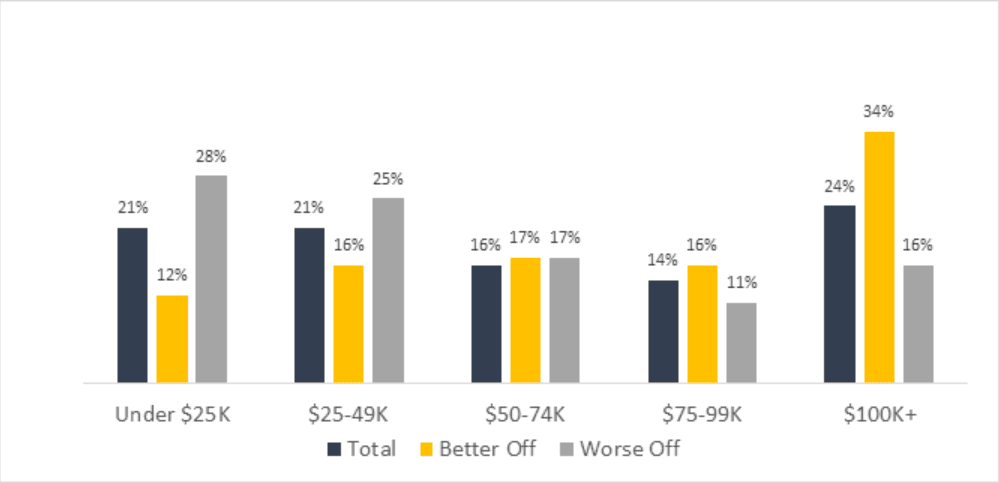

Employment also shows that these two groups are very different. Given age differences, it is not surprising to find that the Worse-Offs are more likely to be retired [32% vs 10%]. But they are also more likely to be unemployed and less likely to like the job they have 25% versus 19% for the Better-Offs.

What really sets these two groups apart is their attitude, when asked about their level of confidence in doing what is needed to meet short term financial goals only 32% of the Worse Offs were completely or fairly confident in comparison to 56% of the Better Offs. Despite this insecurity Worse Offs are still LESS likely to carry debt than their optimistic counterparts. Fifty-four percent of the Better-Offs said they carry a balance, while only 51% of the Worse-Offs do. Surprisingly Better-Offs are also more likely to file for unemployment at 32% versus 23%, but other savings behaviors are the opposite. Cutting back on expenses, spending down savings, and selling things are more likely to happen with Worse-Offs than Better-Offs.

When asked how they feel about dealing with other financial setbacks such as unexpected minor repairs, only 27% of the Worse-Offs feel completely or fairly confident they can deal with the unexpected repair vs. 57% of the Better-Offs. But much like the previous example when asked about borrowing money and withdrawing money from a retirement account, Better-Offs are more likely to do both showing that they have a very different attitude about HOW to deal with these financial challenges.

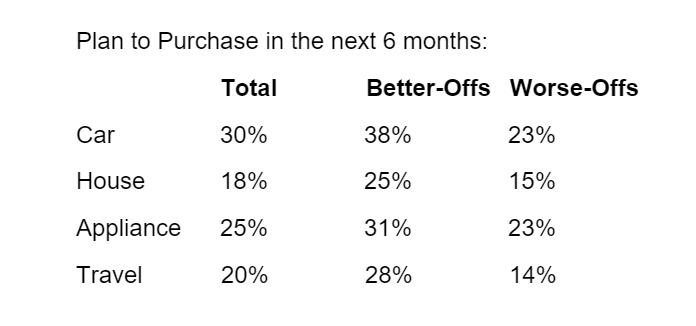

This confidence extends into buying behavior too. Better-Offs are almost TWICE as likely to say they will make some sort of purchase in the next six months. Even when compared to the general population, Better-Offs are ready to spend, as shown in the table below. However, over half of the Worse-Offs do not plan to make ANY large purchases compared to only 28% of the Better-Offs.

We also measured the perceptions of rising prices in goods and services. Worse-Offs are much more likely to think that food, packaged goods, and Household Services have increased, while the Better-Offs are more likely to stay that childcare services prices have gone up.

For anyone with goods and services to sell, the Better-Offs are by all means your target. Not only do they feel better about their situation, but they are ready to purchase and comfortable with managing their debt.

But which consumers are likely to be in your better off or worse off-target audience? Contact us to find out!

To learn more, visit Causeway Solutions to get started!